Tuesday 11th March 2025: Asia-Pacific Markets Decline Amid U.S. Recession Fears

By IC Markets

Asian Stock Markets : Nikkei down 0.71%, Shanghai Composite down 0.32%, Hang Seng down 0.81% ASX down 0.91%

Commodities : Gold at $2902.35 (0.10%), Silver at $32.5 (0.18%), Brent Oil at $69.25 (-0.05%), WTI Oil at $65.88 (-0.14%)

Rates : US 10-year yield at 4.183, UK 10-year yield at 4.645, Germany 10-year yield at 2.8250

IC Markets Europe Fundamental Forecast | 4 March 2025

By IC Markets

After unexpectedly falling in December to mark the first decline in nine months, consumer spending rebounded in January as sales increased 0.3% MoM. The upturn was supported by an increase in categories such as cafes, restaurants and takeaway food services; food retailing; and clothing, footwear and personal accessory retailing.

IC Markets Europe Fundamental Forecast | 27 February 2025

By IC Markets

What happened in the Asia session?

With no major data releases, it was a fairly quiet session as the dollar index (DXY) edged higher towards 106.80 while spot prices for gold fell under $2,900/oz by midday in Asia. Crude oil prices remained under intense overhead pressures with WTI oil hovering above $68.50 per barrel as a potential peace deal between Russia and Ukraine lingers in the background.

Monday 24th February 2025: Technical Outlook and Review

By IC Markets

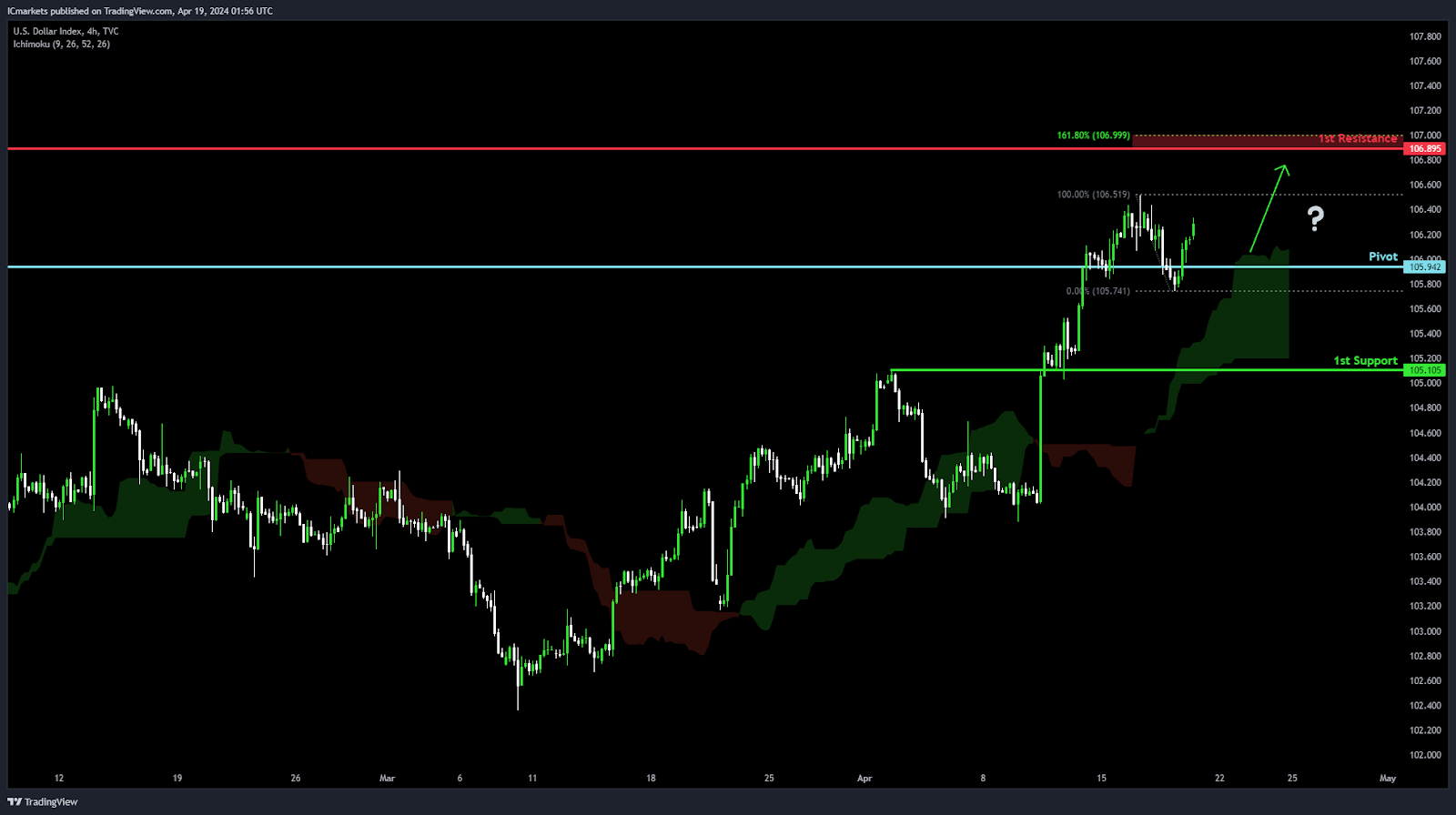

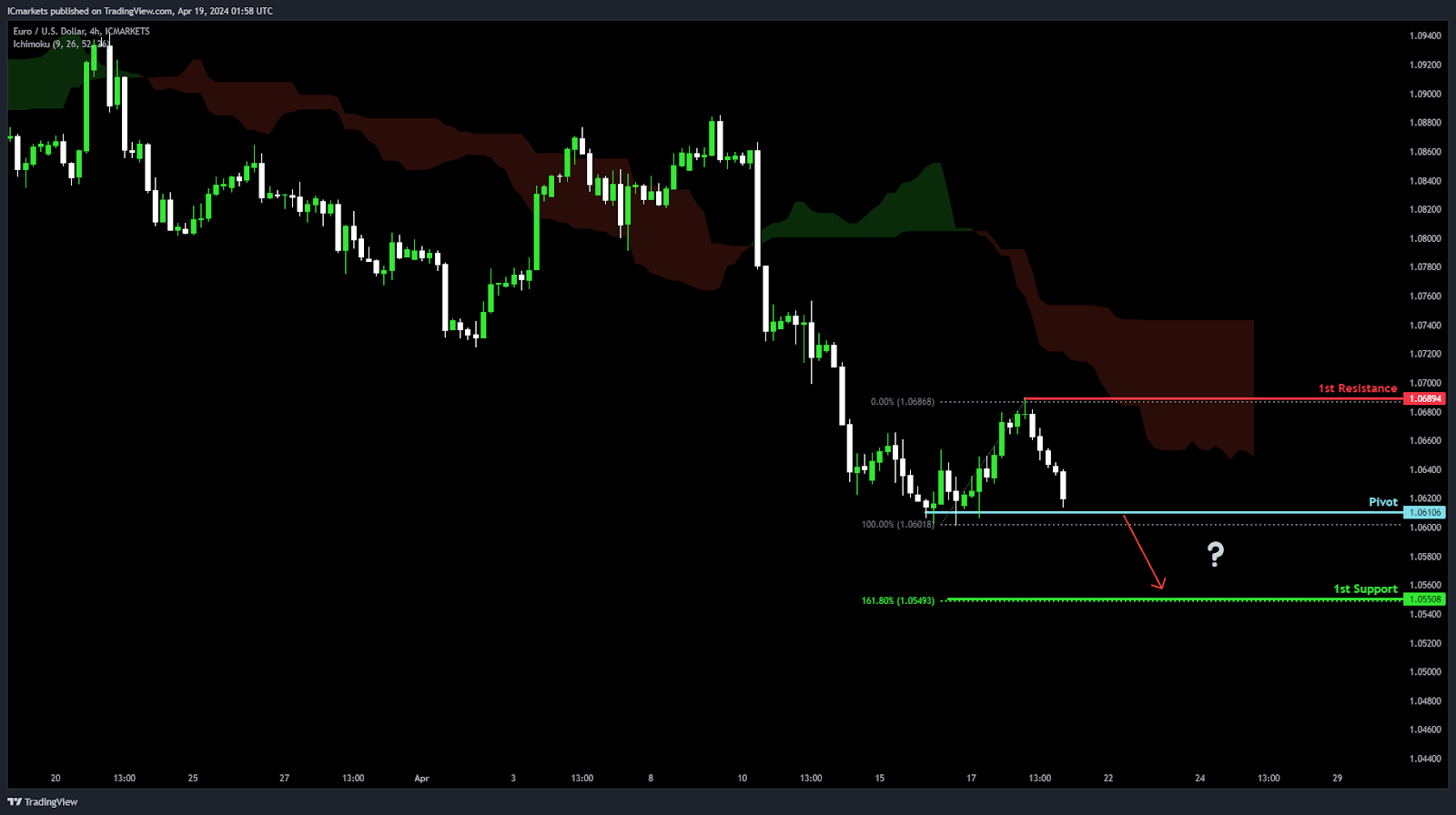

[b]DXY (US Dollar Index):[/b]

Potential Direction: Bearish

Overall momentum of the chart: Bearish

Price could potentially make a short-term rise toward the pivot before reversing and falling toward the 1st support. Also, price has crossed below the Ichimoku cloud, signaling a shift to the downside.

Pivot: 107.49

Supporting reasons: Identified as an overlap resistance, indicating a potential area where selling pressure could emerge.

1st support: 105.44

Supporting reasons: Identified as an overlap support that aligns with the 50% Fibonacci retracement and the 161.8% Fibonacci extension, forming a strong Fibonacci confluence where price could find support.

1st resistance: 108.67

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could cap further upward movement.

IC Markets Europe Fundamental Forecast | 17 February 2025

By IC Markets

What happened in the Asia session?

Wednesday 12th February 2025: Asia-Pacific Markets Mixed as Investors Weigh Tariffs and Fed Policy

By IC Markets

Global Markets:

Asian Stock Markets : Nikkei up 0.29%, Shanghai Composite up 0.01%, Hang Seng up 1.56% ASX up 0.6%

Commodities : Gold at $2910.35 (-0.73%), Silver at $32.15 (-0.48%), Brent Oil at $76.19 (0.39%), WTI Oil at $73.00 (-0.43%)

Rates : US 10-year yield at 4.4550, UK 10-year yield at 4.506, Germany 10-year yield at 2.427

News & Data:

(CAD) Building Permits m/m 11.0% to 1.6% expected

Markets Update:

Asia-Pacific markets traded mixed on Wednesday as investors assessed the impact of U.S. President Donald Trump’s tariffs on regional economies. Meanwhile, U.S. Federal Reserve Chair Jerome Powell reiterated the central bank’s focus on controlling inflation and emphasized that policymakers were in no rush to lower interest rates.

In regional markets, Australia’s S&P/ASX 200 rose 0.5%, while Japan’s Nikkei 225 gained 0.23% after resuming trading post-holiday. However, the Topix dipped 0.2%. South Korea’s Kospi climbed 0.31%, whereas the small-cap Kosdaq declined 0.64%. Hong Kong’s Hang Seng Index surged 1.56%, but mainland China’s CSI 300 slipped 0.13% in volatile trading. India is set to release its January inflation data, with the Nifty 50 opening 0.94% lower and the BSE Sensex falling 0.97%. Investors also await SoftBank Group’s fiscal third-quarter earnings later today.

U.S. markets closed mixed overnight. The S&P 500 edged up 0.03% to 6,068.50, while the Nasdaq Composite dropped 0.36% to 19,643.86. The Dow Jones Industrial Average gained 123.24 points, or 0.28%, to 44,593.65. Powell’s testimony comes amid political uncertainty, as Trump pushes for tariffs on trading partners, creating uncertainty about the administration’s stance toward the Fed.

Powell reaffirmed that the current policy stance, with the benchmark Fed funds rate set between 4.25% and 4.5%, offers flexibility. The Federal Open Market Committee left rates unchanged in its late-January meeting, signaling a cautious approach to monetary policy amid ongoing economic and political uncertainties.

Upcoming Events:

01:30 PM GMT – USD Core CPI m/m

01:30 PM GMT – USD CPI m/m

01:30 PM GMT – USD CPI y/y

Global Markets:

Asian Stock Markets : Nikkei up 0.29%, Shanghai Composite up 0.01%, Hang Seng up 1.56% ASX up 0.6%

Commodities : Gold at $2910.35 (-0.73%), Silver at $32.15 (-0.48%), Brent Oil at $76.19 (0.39%), WTI Oil at $73.00 (-0.43%)

Rates : US 10-year yield at 4.4550, UK 10-year yield at 4.506, Germany 10-year yield at 2.427

News & Data:

(CAD) Building Permits m/m 11.0% to 1.6% expected

Markets Update:

Asia-Pacific markets traded mixed on Wednesday as investors assessed the impact of U.S. President Donald Trump’s tariffs on regional economies. Meanwhile, U.S. Federal Reserve Chair Jerome Powell reiterated the central bank’s focus on controlling inflation and emphasized that policymakers were in no rush to lower interest rates.

In regional markets, Australia’s S&P/ASX 200 rose 0.5%, while Japan’s Nikkei 225 gained 0.23% after resuming trading post-holiday. However, the Topix dipped 0.2%. South Korea’s Kospi climbed 0.31%, whereas the small-cap Kosdaq declined 0.64%. Hong Kong’s Hang Seng Index surged 1.56%, but mainland China’s CSI 300 slipped 0.13% in volatile trading. India is set to release its January inflation data, with the Nifty 50 opening 0.94% lower and the BSE Sensex falling 0.97%. Investors also await SoftBank Group’s fiscal third-quarter earnings later today.

U.S. markets closed mixed overnight. The S&P 500 edged up 0.03% to 6,068.50, while the Nasdaq Composite dropped 0.36% to 19,643.86. The Dow Jones Industrial Average gained 123.24 points, or 0.28%, to 44,593.65. Powell’s testimony comes amid political uncertainty, as Trump pushes for tariffs on trading partners, creating uncertainty about the administration’s stance toward the Fed.

Powell reaffirmed that the current policy stance, with the benchmark Fed funds rate set between 4.25% and 4.5%, offers flexibility. The Federal Open Market Committee left rates unchanged in its late-January meeting, signaling a cautious approach to monetary policy amid ongoing economic and political uncertainties.

Upcoming Events:

01:30 PM GMT – USD Core CPI m/m

01:30 PM GMT – USD CPI m/m

01:30 PM GMT – USD CPI y/yMonday 10th February 2025: Markets Mixed Amid Trade Tensions and Inflation Worries

By IC Markets

Global Markets:

Asian Stock Markets : Nikkei down 0.13%, Shanghai Composite up 0.61%, Hang Seng up 1.86% ASX down 0.34%

Commodities : Gold at $2915.35 (0.93%), Silver at $32.75 (0.38%), Brent Oil at $75.19 (0.69%), WTI Oil at $71.54 (0.73%)

Rates : US 10-year yield at 4.487, UK 10-year yield at 4.476, Germany 10-year yield at 2.377

News & Data:

(CAD) Unemployment Rate 6.60% to 6.80% expected

(CAD) Employment Change 76.0K vs 25.5K expected

(USD) Non-Farm Employment Change 143K vs 169K expected

Markets Update:

Asia-Pacific markets showed mixed performance on Monday as rising trade tensions kept investors cautious. U.S. President Donald Trump stated he planned to impose a 25% tariff on all steel and aluminum imports, fueling market uncertainty. Japan’s Nikkei 225 closed flat at 38,801.17, while the Topix index edged down 0.15% to 2,733.01. The country’s loan growth slowed to 3% in January from December’s 3.1%. South Korea’s Kospi remained unchanged at 2,521.27, but the Kosdaq gained 0.91% to 749.67.

Hong Kong’s Hang Seng index rose 1.67%, and China’s CSI 300 gained 0.11% after earlier losses. China’s consumer inflation hit a five-month high in January due to Lunar New Year spending, with the CPI rising 0.7% monthly and 0.5% annually, surpassing Reuters’ 0.4% estimate. Meanwhile, the producer price index fell 2.3% annually, exceeding the expected 2.1% drop. Indian markets extended losses from Friday after the Reserve Bank of India’s unexpected interest rate cut. The Nifty 50 fell 0.94%, while the BSE Sensex dropped 0.83%.

Singapore’s Straits Times Index hit a record high of 3,910.12 points, driven by gains in Singtel and major banks. The STI was up 0.68%. Australia’s S&P/ASX 200 fell 0.34% to 8,482.80. The three key U.S. indexes fell Friday after Trump’s tariff announcement and inflation concerns. Markets were further pressured by consumer sentiment and jobs data, which pointed to rising inflation and pushed the 10-year Treasury yield above 4.5% at its session high.

The Dow Jones Industrial Average lost 444.23 points, or 0.99%, to close at 44,303.40. The S&P 500 declined 0.95% to 6,025.99, and the Nasdaq Composite slid 1.36% to 19,523.40. Friday’s losses pushed major indexes into negative territory for the week.

Upcoming Events:

02:00 PM GMT – EUR ECB President Lagarde Speaks

Global Markets:

Asian Stock Markets : Nikkei down 0.13%, Shanghai Composite up 0.61%, Hang Seng up 1.86% ASX down 0.34%

Commodities : Gold at $2915.35 (0.93%), Silver at $32.75 (0.38%), Brent Oil at $75.19 (0.69%), WTI Oil at $71.54 (0.73%)

Rates : US 10-year yield at 4.487, UK 10-year yield at 4.476, Germany 10-year yield at 2.377

News & Data:

(CAD) Unemployment Rate 6.60% to 6.80% expected

(CAD) Employment Change 76.0K vs 25.5K expected

(USD) Non-Farm Employment Change 143K vs 169K expected

Markets Update:

Asia-Pacific markets showed mixed performance on Monday as rising trade tensions kept investors cautious. U.S. President Donald Trump stated he planned to impose a 25% tariff on all steel and aluminum imports, fueling market uncertainty. Japan’s Nikkei 225 closed flat at 38,801.17, while the Topix index edged down 0.15% to 2,733.01. The country’s loan growth slowed to 3% in January from December’s 3.1%. South Korea’s Kospi remained unchanged at 2,521.27, but the Kosdaq gained 0.91% to 749.67.

Hong Kong’s Hang Seng index rose 1.67%, and China’s CSI 300 gained 0.11% after earlier losses. China’s consumer inflation hit a five-month high in January due to Lunar New Year spending, with the CPI rising 0.7% monthly and 0.5% annually, surpassing Reuters’ 0.4% estimate. Meanwhile, the producer price index fell 2.3% annually, exceeding the expected 2.1% drop. Indian markets extended losses from Friday after the Reserve Bank of India’s unexpected interest rate cut. The Nifty 50 fell 0.94%, while the BSE Sensex dropped 0.83%.

Singapore’s Straits Times Index hit a record high of 3,910.12 points, driven by gains in Singtel and major banks. The STI was up 0.68%. Australia’s S&P/ASX 200 fell 0.34% to 8,482.80. The three key U.S. indexes fell Friday after Trump’s tariff announcement and inflation concerns. Markets were further pressured by consumer sentiment and jobs data, which pointed to rising inflation and pushed the 10-year Treasury yield above 4.5% at its session high.

The Dow Jones Industrial Average lost 444.23 points, or 0.99%, to close at 44,303.40. The S&P 500 declined 0.95% to 6,025.99, and the Nasdaq Composite slid 1.36% to 19,523.40. Friday’s losses pushed major indexes into negative territory for the week.

Upcoming Events:

02:00 PM GMT – EUR ECB President Lagarde SpeaksWednesday 5th February 2025: Asia-Pacific Markets Mixed as Wall Street Rallies Amid Trade Tensions

By IC Markets

Global Markets:

- Asian Stock Markets : Nikkei up 0.12%, Shanghai Composite down 0.83%, Hang Seng down 1.13% ASX up 0.5%

- Commodities : Gold at $2887.35 (0.43%), Silver at $32.95 (-0.28%), Brent Oil at $76.59 (-0.19%), WTI Oil at $72.64 (-0.13%)

- Rates : US 10-year yield at 4.512, UK 10-year yield at 4.5210, Germany 10-year yield at 2.392

News & Data:

- (USD) JOLTS Job opening 7.60M vs 8.01M expected

Markets Update:

Asia-Pacific markets were mixed Wednesday as Wall Street gained overnight, shrugging off Trump’s tariffs and China’s retaliatory measures. China resumed trading after the Lunar New Year break, with investors closely monitoring its response to U.S. duties. Morningstar’s Asia equity analyst Kai Wang noted that China’s tariffs on U.S. imports are largely symbolic, affecting only 12% of total imports. While the immediate risk appears limited, uncertainties remain as trade tensions could escalate given Trump’s unpredictable stance, keeping market volatility a key concern.

Mainland China’s CSI300 Index opened higher but later declined 0.27%, while the Caixin Services PMI fell to 51.0 in January from 52.2 in December, indicating a slowdown in services activity. Hong Kong’s Hang Seng dropped 0.69%, reversing previous gains. In Japan, the Nikkei 225 edged down 0.12%, with the broader Topix index remaining flat. South Korea’s Kospi climbed 1.16%, while the Kosdaq advanced 1.31%. The country’s January consumer price index rose 0.7% month-on-month and 2.2% year-on-year, exceeding expectations.

Indian markets saw modest gains as investors awaited the Reserve Bank of India’s monetary policy decision, anticipating a rate cut. The Nifty 50 rose 0.11%, while the BSE Sensex inched up 0.15%. Meanwhile, Australia’s S&P/ASX 200 gained 0.61%, tracking overall regional movements.

In the U.S., markets closed higher, fueled by strong earnings reports. Palantir surged 24% on solid quarterly results, while Nvidia rose 1.7%. The Nasdaq Composite jumped 1.35% to 19,654.02, the S&P 500 climbed 0.72% to 6,037.88, and the Dow Jones gained 134.13 points to close at 44,556.04.

Upcoming Events:

- 03:00 PM GMT – USD ISM Services PMI

- 02:45 PM GMT – USD Final Services PMI

Global Markets:

- Asian Stock Markets : Nikkei up 0.12%, Shanghai Composite down 0.83%, Hang Seng down 1.13% ASX up 0.5%

- Commodities : Gold at $2887.35 (0.43%), Silver at $32.95 (-0.28%), Brent Oil at $76.59 (-0.19%), WTI Oil at $72.64 (-0.13%)

- Rates : US 10-year yield at 4.512, UK 10-year yield at 4.5210, Germany 10-year yield at 2.392

News & Data:

- (USD) JOLTS Job opening 7.60M vs 8.01M expected

Markets Update:

Asia-Pacific markets were mixed Wednesday as Wall Street gained overnight, shrugging off Trump’s tariffs and China’s retaliatory measures. China resumed trading after the Lunar New Year break, with investors closely monitoring its response to U.S. duties. Morningstar’s Asia equity analyst Kai Wang noted that China’s tariffs on U.S. imports are largely symbolic, affecting only 12% of total imports. While the immediate risk appears limited, uncertainties remain as trade tensions could escalate given Trump’s unpredictable stance, keeping market volatility a key concern.

Mainland China’s CSI300 Index opened higher but later declined 0.27%, while the Caixin Services PMI fell to 51.0 in January from 52.2 in December, indicating a slowdown in services activity. Hong Kong’s Hang Seng dropped 0.69%, reversing previous gains. In Japan, the Nikkei 225 edged down 0.12%, with the broader Topix index remaining flat. South Korea’s Kospi climbed 1.16%, while the Kosdaq advanced 1.31%. The country’s January consumer price index rose 0.7% month-on-month and 2.2% year-on-year, exceeding expectations.

Indian markets saw modest gains as investors awaited the Reserve Bank of India’s monetary policy decision, anticipating a rate cut. The Nifty 50 rose 0.11%, while the BSE Sensex inched up 0.15%. Meanwhile, Australia’s S&P/ASX 200 gained 0.61%, tracking overall regional movements.

In the U.S., markets closed higher, fueled by strong earnings reports. Palantir surged 24% on solid quarterly results, while Nvidia rose 1.7%. The Nasdaq Composite jumped 1.35% to 19,654.02, the S&P 500 climbed 0.72% to 6,037.88, and the Dow Jones gained 134.13 points to close at 44,556.04.

Upcoming Events:

- 03:00 PM GMT – USD ISM Services PMI

- 02:45 PM GMT – USD Final Services PMIMonday 27th January 2025: Asian Markets Mixed as Investors Assess China’s Economic Data

By IC Markets

Global Markets:

- Asian Stock Markets : Nikkei down 1.01%, Shanghai Composite up 0.12%, Hang Seng up 0.84% ASX up 0.36%

- Commodities : Gold at $2786.35 (-0.76%), Silver at $30.65 (-1.48%), Brent Oil at $76.39 (-0.89%), WTI Oil at $74.04 (-0.83%)

- Rates : US 10-year yield at 4.586, UK 10-year yield at 4.6305, Germany 10-year yield at 2.5445

News & Data:

- (USD) Flash Manufacturing PMI 50.1 vs 49.8 expected

- (USD) Flash Services PMI 52.8 vs 56.4 expected

Markets Update:

Asian markets showed mixed movements on Monday as investors reacted to China’s manufacturing and industrial profit data. Japan’s Nikkei 225 slipped 0.14%, while the Topix gained 0.68%. Chip-related stocks in Japan saw significant declines, with Advantest plunging 8.2%, Tokyo Electron losing 4.53%, and Renesas Electronics edging down 0.19%. The drop came amid concerns over Chinese AI startup DeepSeek’s open-source large-language model, seen as a potential challenge to U.S. dominance in AI technology.

In Hong Kong, the Hang Seng Index rose 0.89% at the open, while mainland China’s CSI 300 added 0.28%. However, China’s manufacturing sector faced a setback, with the January Purchasing Managers’ Index unexpectedly contracting to 49.1, below the forecasted 50.1. Despite this, December’s industrial profits in China jumped 11% year-over-year, offering some optimism amid broader economic challenges. Markets in Australia, Taiwan, and South Korea were closed for holidays.

To support its ailing stock market, China’s Securities Regulatory Commission (CSRC) announced measures to promote index investment products, including equity and bond ETFs. These initiatives, unveiled on Sunday, build on earlier efforts urging state-owned mutual funds and insurers to increase their equity holdings. Hong Kong, meanwhile, is set to release December trade data, which could further impact regional market sentiment.

In the U.S., markets ended a strong week on a softer note. The S&P 500 fell 0.3% to 6,101.24, the Nasdaq Composite lost 0.5% to 19,954.30, and the Dow Jones Industrial Average declined 140.82 points to 44,424.25. Investor enthusiasm surrounding Donald Trump’s return to the White House drove risk assets higher, with all three major indexes posting their second straight weekly gains, signaling renewed bullish momentum.

Upcoming Events:

03:00 PM GMT – USD New Home Sales

Global Markets:

- Asian Stock Markets : Nikkei down 1.01%, Shanghai Composite up 0.12%, Hang Seng up 0.84% ASX up 0.36%

- Commodities : Gold at $2786.35 (-0.76%), Silver at $30.65 (-1.48%), Brent Oil at $76.39 (-0.89%), WTI Oil at $74.04 (-0.83%)

- Rates : US 10-year yield at 4.586, UK 10-year yield at 4.6305, Germany 10-year yield at 2.5445

News & Data:

- (USD) Flash Manufacturing PMI 50.1 vs 49.8 expected

- (USD) Flash Services PMI 52.8 vs 56.4 expected

Markets Update:

Asian markets showed mixed movements on Monday as investors reacted to China’s manufacturing and industrial profit data. Japan’s Nikkei 225 slipped 0.14%, while the Topix gained 0.68%. Chip-related stocks in Japan saw significant declines, with Advantest plunging 8.2%, Tokyo Electron losing 4.53%, and Renesas Electronics edging down 0.19%. The drop came amid concerns over Chinese AI startup DeepSeek’s open-source large-language model, seen as a potential challenge to U.S. dominance in AI technology.

In Hong Kong, the Hang Seng Index rose 0.89% at the open, while mainland China’s CSI 300 added 0.28%. However, China’s manufacturing sector faced a setback, with the January Purchasing Managers’ Index unexpectedly contracting to 49.1, below the forecasted 50.1. Despite this, December’s industrial profits in China jumped 11% year-over-year, offering some optimism amid broader economic challenges. Markets in Australia, Taiwan, and South Korea were closed for holidays.

To support its ailing stock market, China’s Securities Regulatory Commission (CSRC) announced measures to promote index investment products, including equity and bond ETFs. These initiatives, unveiled on Sunday, build on earlier efforts urging state-owned mutual funds and insurers to increase their equity holdings. Hong Kong, meanwhile, is set to release December trade data, which could further impact regional market sentiment.

In the U.S., markets ended a strong week on a softer note. The S&P 500 fell 0.3% to 6,101.24, the Nasdaq Composite lost 0.5% to 19,954.30, and the Dow Jones Industrial Average declined 140.82 points to 44,424.25. Investor enthusiasm surrounding Donald Trump’s return to the White House drove risk assets higher, with all three major indexes posting their second straight weekly gains, signaling renewed bullish momentum.

Upcoming Events:

03:00 PM GMT – USD New Home SalesIC Markets Europe Fundamental Forecast | 30 December 2024

By IC Markets

What happened in the Asia session?

Japan’s manufacturing sector has remained in contraction since July with the final PMI reading of 49.6 for December indicating no change to this trend. This sector saw softer deterioration in manufacturing conditions at the end of 2024 as production and demand fell slower than expected while there was a renewed increase in employment. The yen remains weak keeping USD/JPY elevated – this currency pair was hovering around 157.80 by midday Asia.

What does it mean for the Europe & US sessions?

After sliding lower over the last couple of months, the Chicago PMI is expected to rebound from 40.2 to 42.7 in December. However, this would still mark a 13th consecutive month of contraction in Chicago’s economic activity. Demand for the dollar could wane should we see this index post a weaker-than-anticipated result.

The Dollar Index (DXY)

Key news events today

Chicago PMI (2:45 pm GMT)

What can we expect from DXY today?

After sliding lower over the last couple of months, the Chicago PMI is expected to rebound from 40.2 to 42.7 in December. However, this would still mark a 13th consecutive month of contraction in Chicago’s economic activity. Demand for the dollar could wane should we see this index post a weaker-than-anticipated result.

Central Bank Notes:

- The Board of Governors of the Federal Reserve System voted by a majority to lower the Federal Funds Rate target range by 25 basis points to 4.25 to 4.50% on 18 December. Voting against the action was Beth M. Hammack, who preferred to maintain the target range at 4.5 to 4.75%.

- The Committee seeks to achieve maximum employment and inflation at the rate of 2% over the longer run and judges that the risks to achieving its employment and inflation goals are roughly in balance.

- The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

- Recent indicators suggest that economic activity has continued to expand at a solid pace while labour market conditions have generally eased, and the unemployment rate has moved up but remains low.

- Inflation has made further progress toward the Committee’s 2% objective but remains somewhat elevated.

- The Summary of Economic Projections (SEP) now indicates just two rate cuts in 2025 totalling 50 bps, compared to the full percentage point of reductions projected in the previous quarter.

- GDP growth forecasts were revised upward for 2024 (2.5% vs to 2% in the September projection) and 2025 (2.1% vs 2%), while remaining steady at 2% for 2026. Similarly, PCE inflation projections have been adjusted higher for 2024 (2.4% vs 2.3%), 2025 (2.5% vs 2.1%), and 2026 (2.1% vs 2%).

- In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.

- In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook and would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.

- In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities. Beginning in June, the Committee slowed the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion.

- The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities.

- The next meeting runs from 28 to 29 January 2025.

Next 24 Hours Bias

Weak Bearish

Gold (XAU)

Key news events today

Chicago PMI (2:45 pm GMT)

What can we expect from Gold today?

After sliding lower over the last couple of months, the Chicago PMI is expected to rebound from 40.2 to 42.7 in December. However, this would still mark a 13th consecutive month of contraction in Chicago’s economic activity. Demand for the dollar could wane should we see this index post a weaker-than-anticipated result – a move that would provide lift for gold prices.

Next 24 Hours Bias

Weak Bullish

The Australian Dollar (AUD)

Key news events today

No major news events.

What can we expect from AUD today?

The Aussie has fallen for five straight weeks to lose nearly 5% over this period. This currency pair opened at 0.6211 to edge towards 0.6230 as Asian markets came online.

Central Bank Notes:

- The RBA kept the cash rate target unchanged at 4.35% on 10 December, marking the ninth consecutive pause.

- Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance. However, measures of underlying inflation are around 3.5%, which is still some way from the 2.5% midpoint of the inflation target.

The most recent forecasts published in the November Statement on Monetary Policy (SMP) do not see inflation returning sustainably to the midpoint of the target until 2026 but the Board is gaining some confidence that inflationary pressures are declining in line with these recent forecasts with risks remaining in place.

- Growth in output has been weak as the economy grew by only 0.8% in the September quarter over the past year. Outside of the COVID-19 pandemic, this was the slowest pace of growth since the early 1990s.

- A range of indicators suggest that labour market conditions remain tight; while those conditions have been easing gradually, some indicators have recently stabilised. The unemployment rate was 4.1 per cent in October, up from 3.5 per cent in late 2022.

- Wage pressures have eased more than expected in the November SMP. The rate of wages growth as measured by the Wage Price Index was 3.5% over the year to the September quarter, a step down from the previous quarter, but labour productivity growth remains weak.

- Sustainably returning inflation to target within a reasonable timeframe remains the Board’s highest priority. This is consistent with the RBA’s mandate for price stability and full employment. To date, longer term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

The Board will continue to rely upon the data and the evolving assessment of risks to guide its decisions, paying close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market.

- The next meeting is on 18 February 2025.

Next 24 Hours Bias

Weak Bullish

The Kiwi Dollar (NZD)

Key news events today

No major news events.

What can we expect from NZD today?

Just like its Pacific neighbour, the Kiwi has depreciated significantly as it tumbled 4.8% over the past four weeks. This currency pair opened at 0.5626 to drift higher at the beginning of the Asia session.

Central Bank Notes:

- The Monetary Policy Committee (MPC) agreed to reduce the Official Cash Rate (OCR) by 50 basis points bringing it down to 4.25% on 27 November, marking the third consecutive rate cut.

- The Committee assessed that annual consumer price inflation has declined and is now close to the midpoint of the MPC’s 1 to 3% target band; inflation expectations are also close to target and core inflation is converging to the midpoint.

- Economic activity remains subdued and output continues to be below its potential. With excess productive capacity in the economy, inflation pressures have eased. If economic conditions continue to evolve as projected, the Committee expects to be able to lower the OCR further early next year.

- Domestic economic activity remains below trend, as a result of weakness in demand for durable goods consumption and investment. This has been reflected in falling activity in interest rate sensitive sectors such as construction, manufacturing, and retail trade. In contrast, some services sectors have continued to grow.

- Consistent with feedback from business visits, high frequency indicators suggest that the economy has stabilised in recent months. Economic growth is expected to recover from the December quarter, in part due to lower interest rates, but there is uncertainty around the exact timing and speed of the recovery.

- Wage growth is slowing, consistent with inflation returning to the target midpoint while employment levels and job vacancies have declined, reflecting subdued economic activity; unemployment is expected to continue rising in the near term.

- Expectations of future inflation, the pricing intentions of firms, and spare productive capacity are consistent with the inflation target being sustainably achieved, providing the context and the confidence for the Committee to further ease monetary policy restraint.

- The next meeting is on 19 February 2025.

Next 24 Hours Bias

Weak Bullish

The Japanese Yen (JPY)

Key news events today

Manufacturing PMI (12:30 am GMT)

What can we expect from JPY today?

Japan’s manufacturing sector has remained in contraction since July with the final PMI reading of 49.6 for December indicating no change to this trend. This sector saw softer deterioration in manufacturing conditions at the end of 2024 as production and demand fell slower than expected while there was a renewed increase in employment. The yen remains weak keeping USD/JPY elevated – this currency pair was hovering around 157.80 by midday Asia.

Central Bank Notes:

- The Policy Board of the Bank of Japan decided on 19 December, by a 8-1 majority vote, to set the following guideline for money market operations for the intermeeting period:

- The Bank will encourage the uncollateralized overnight call rate to remain at around 0.25%.

- The Bank will embark on a plan to reduce the amount of its monthly outright purchases of JGBs so that it will be about 3 trillion yen in January-March 2026; the amount will be cut down by about 400 billion yen each calendar quarter in principle.

- Japan’s economy has recovered moderately, although some weakness has been seen in part. Exports and industrial production have been more or less flat while corporate profits have been on an improving trend and business sentiment has stayed at a favourable level.

- The employment and income situation has improved moderately while private consumption has been on a moderate increasing trend despite the impact of price rises and other factors.

- On the price front, the year-on-year rate of increase in the consumer price index (CPI, all items less fresh food) has been in the range of 2.0-2.5% recently, as services prices have continued to rise moderately, reflecting factors such as wage increases, although the effects of a passthrough to consumer prices of cost increases led by the past rise in import prices have waned; inflation expectations have risen moderately.

- With regard to the CPI (all items less fresh food), while the effects of the pass-through to consumer prices of cost increases led by the past rise in import prices are expected to wane, underlying CPI inflation is expected to increase gradually, since it is projected that the output gap will improve and that medium- to long-term inflation expectations will rise with a virtuous cycle between wages and prices continuing to intensify.

- Japan’s economy is likely to keep growing at a pace above its potential growth rate, with overseas economies continuing to grow moderately and as a virtuous cycle from income to spending gradually intensifies against the background of factors such as accommodative financial conditions.

- The next meeting is on 24 January 2025.

Next 24 Hours Bias

Weak Bearish

The Euro (EUR)

Key news events today

No major news events.

What can we expect from EUR today?

The Euro has tumbled nearly 1.3% over the last three weeks as it looks to re-test its 52-week low at 1.0331. This currency pair opened at 1.0426 and was edging higher towards 1.0440 as Asian markets came online.

Central Bank Notes:

- The Governing Council reduced the three key ECB interest rates by 25 basis points on 12 December to mark the third successive rate cut.

- Accordingly, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be decreased to 3.15%, 3.40% and 3.00% respectively.

- The disinflation process is well on track and most measures of underlying inflation suggest that inflation will settle at around the Governing Council’s 2% medium-term target on a sustained basis.

- Staff see headline inflation averaging 2.4% in 2024, 2.1% in 2025, 1.9% in 2026 and 2.1% in 2027 when the expanded EU Emissions Trading System becomes operational. For inflation excluding energy and food, staff project an average of 2.9% in 2024, 2.3% in 2025 and 1.9% in both 2026 and 2027.

- Staff now expect a slower economic recovery than in the September projections. Although growth picked up in the third quarter of this year, survey indicators suggest it has slowed in the current quarter – the economy is expected to grow by 0.7% in 2024, 1.1% in 2025, 1.4% in 2026 and 1.3% in 2027

- The Eurosystem no longer reinvests all of the principal payments from maturing securities purchased under the pandemic emergency purchase programme (PEPP), reducing the PEPP portfolio by €7.5 billion per month on average and the Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

- The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises sustainably at its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission.

- The next meeting is on 30 January 2025.

Next 24 Hours Bias

Weak Bullish

The Swiss Franc (CHF)

Key news events today

No major news events.

What can we expect from CHF today?

The franc has weakened significantly since the end of September with UDS/CHF rallying almost 7.5% over this period. This currency pair opened at 0.9010 before drifting lower at the beginning of the Asia session.

Central Bank Notes:

-The SNB eased monetary policy by lowering its key policy rate by 50 basis points, going from 1.00% to 0.50% on 12 December, marking for the fourth consecutive reduction.

Underlying inflationary pressure has decreased again this quarter.

- Inflation in the period since the last monetary policy assessment has again been lower than expected as it decreased from 1.1% in August to 0.7% in November; both goods and services contributed to this decline.

- In the shorter term, the new conditional inflation forecast is below that of September: 1.1% for 2024, 0.3% for 2025 and 0.8% for 2026, based on the assumption that the SNB policy rate is 0.5% over the entire forecast horizon.

- GDP growth in Switzerland was only modest in the third quarter of 2024 with growth in the services sector was again somewhat stronger, while value added in manufacturing declined.

- There was a further slight increase in unemployment, and employment growth was subdued while the utilisation of overall production capacity was

normal.

- The SNB anticipates GDP growth of around 1% this year while currently expecting growth of between 1.0% and 1.5% for 2025.

- The SNB will continue to monitor the situation closely, and will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term.

- The next meeting is on 20 March 2025.

Next 24 Hours Bias

Weak Bearish

The Pound (GBP)

Key news events today

No major news events.

What can we expect from GBP today?

Just like many other currencies, the Pound has devalued strongly in the last quarter of this year with Cable breaking under the threshold of 1.2500 on 20th December. This currency pair opened at 1.2572 and was hovering around this level as Asian markets came online.

Central Bank Notes:

- The Bank of England’s Monetary Policy Committee (MPC) voted by a majority of 6 to 3 to maintain the Bank Rate at 4.75% on 19 December 2024 – three members preferred to reduce the Bank rate by 25 basis points, bringing it down to 4.50%.

- The MPC also voted unanimously to reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100B over the next 12 months to a total of £558B, starting in October 2024. On 18 December 2024, the stock of UK government bonds held for monetary policy purposes was £655B.

- Twelve-month CPI inflation had increased to 2.6% in November from 1.7% in September, slightly higher than previous expectations while services consumer price inflation had remained elevated, at 5.0%, while core goods price inflation had risen to 1.1%.

- Headline CPI inflation was slightly higher than previous expectations, owing in large part to stronger inflation in core goods and food, and is expected to continue to rise slightly in the near term.

- Most indicators of UK near-term activity have declined with Bank staff expecting GDP growth to be weaker at the end of the year than originally projected in the November Monetary Policy Report.

- Bank staff now expected zero GDP growth in 2024 Q4, weaker than the 0.3% that had been incorporated in the November Report, broadly consistent with the latest combined steer from business surveys and the available official data.

- The Committee now judges that the labour market is broadly in balance as annual private sector regular average weekly earnings growth picked up quite sharply in the three months to October but there remains significant uncertainty around developments in the labour market.

- Monetary policy has been guided by the need to squeeze remaining inflationary pressures out of the economy to achieve the 2% target both in a timely manner and on a lasting basis. Over recent quarters there has been progress in disinflation, particularly as previous external shocks have abated, although remaining domestic inflationary pressures are resolving more slowly.

- The Committee continues to monitor closely the risks of inflation persistence and will assess the extent to which the evolving evidence is consistent with more constrained supply, which could sustain inflationary pressures, or with weaker demand, which could lead to the emergence of spare capacity in the economy and push down inflation; a gradual approach to removing monetary policy restraint remains appropriate.

- Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further and the Committee will decide the appropriate degree of monetary policy restrictiveness at each meeting.

- The next meeting is on 6 February 2025.

Next 24 Hours Bias

Weak Bullish

The Canadian Dollar (CAD)

Key news events today

No major news events.

What can we expect from CAD today?

The Loonie has been one of the weakest currencies in 2024 causing USD/CAD to surge beyond 1.4450 in recent weeks. This currency pair opened at 1.4413 and is likely to remain elevated as the day progresses.

Central Bank Notes:

- The Bank of Canada reduced its target for the overnight rate by 50 basis points bringing it down to 3.25% while continuing its policy of balance sheet normalization on 11 December; this marked the fifth consecutive meeting where rates were reduced.

- Canada’s economy grew by 1% in the third quarter, somewhat below the Bank’s October projection, and the fourth quarter also looks weaker than projected. Third-quarter GDP growth was pulled down by business investment, inventories and exports.

- The unemployment rate rose to 6.8% in November as employment continued to grow more slowly than the labour force while wage growth showed some signs of easing, but remains elevated relative to productivity.

- Headline CPI has declined significantly from 2.7% in June to 1.6% in September while shelter costs inflation remains elevated but has begun to ease; the preferred measures of core inflation are now below 2.5%.

- CPI inflation has been about 2% since the summer, and is expected to average close to the 2% target over the next couple of years. Since October, the upward pressure on inflation from shelter and the downward pressure from goods prices have both moderated as expected.

- Looking ahead, the GST holiday will temporarily lower inflation but that will be unwound once the GST break ends. In addition, the possibility the incoming US administration will impose new tariffs on Canadian exports to the United States has increased uncertainty and clouded the economic outlook

- With inflation around 2%, the economy in excess supply, and recent indicators tilted towards softer growth than projected, the Governing Council decided to reduce the policy rate by a further 50 basis points to support growth and keep inflation close to the middle of the 1-3% target range.

- The Governing Council has reduced the policy rate substantially since June and going forward, they will be evaluating the need for further reductions in the policy rate one decision at a time.

- The Bank is committed to maintaining price stability for Canadians by keeping inflation close to the 2% target.

- The next meeting is on 29 January 2025.

Next 24 Hours Bias

Weak Bullish

Oil

Key news events today

No major news events.

What can we expect from Oil today?

After Friday’s larger-than-expected drawdown in the EIA inventories, crude oil prices are likely to remain buoyed on Monday. WTI oil was hovering around $70.50 per barrel as markets re-opened and this benchmark could continue its upward ascent towards the $72-mark.

Next 24 Hours Bias

Weak Bullish

What happened in the Asia session?

Japan’s manufacturing sector has remained in contraction since July with the final PMI reading of 49.6 for December indicating no change to this trend. This sector saw softer deterioration in manufacturing conditions at the end of 2024 as production and demand fell slower than expected while there was a renewed increase in employment. The yen remains weak keeping USD/JPY elevated – this currency pair was hovering around 157.80 by midday Asia.

What does it mean for the Europe & US sessions?

After sliding lower over the last couple of months, the Chicago PMI is expected to rebound from 40.2 to 42.7 in December. However, this would still mark a 13th consecutive month of contraction in Chicago’s economic activity. Demand for the dollar could wane should we see this index post a weaker-than-anticipated result.

The Dollar Index (DXY)

Key news events today

Chicago PMI (2:45 pm GMT)

What can we expect from DXY today?

After sliding lower over the last couple of months, the Chicago PMI is expected to rebound from 40.2 to 42.7 in December. However, this would still mark a 13th consecutive month of contraction in Chicago’s economic activity. Demand for the dollar could wane should we see this index post a weaker-than-anticipated result.

Central Bank Notes:

- The Board of Governors of the Federal Reserve System voted by a majority to lower the Federal Funds Rate target range by 25 basis points to 4.25 to 4.50% on 18 December. Voting against the action was Beth M. Hammack, who preferred to maintain the target range at 4.5 to 4.75%.

- The Committee seeks to achieve maximum employment and inflation at the rate of 2% over the longer run and judges that the risks to achieving its employment and inflation goals are roughly in balance.

- The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

- Recent indicators suggest that economic activity has continued to expand at a solid pace while labour market conditions have generally eased, and the unemployment rate has moved up but remains low.

- Inflation has made further progress toward the Committee’s 2% objective but remains somewhat elevated.

- The Summary of Economic Projections (SEP) now indicates just two rate cuts in 2025 totalling 50 bps, compared to the full percentage point of reductions projected in the previous quarter.

- GDP growth forecasts were revised upward for 2024 (2.5% vs to 2% in the September projection) and 2025 (2.1% vs 2%), while remaining steady at 2% for 2026. Similarly, PCE inflation projections have been adjusted higher for 2024 (2.4% vs 2.3%), 2025 (2.5% vs 2.1%), and 2026 (2.1% vs 2%).

- In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.

- In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook and would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.

- In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities. Beginning in June, the Committee slowed the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion.

- The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities.

- The next meeting runs from 28 to 29 January 2025.

Next 24 Hours Bias

Weak Bearish

Gold (XAU)

Key news events today

Chicago PMI (2:45 pm GMT)

What can we expect from Gold today?

After sliding lower over the last couple of months, the Chicago PMI is expected to rebound from 40.2 to 42.7 in December. However, this would still mark a 13th consecutive month of contraction in Chicago’s economic activity. Demand for the dollar could wane should we see this index post a weaker-than-anticipated result – a move that would provide lift for gold prices.

Next 24 Hours Bias

Weak Bullish

The Australian Dollar (AUD)

Key news events today

No major news events.

What can we expect from AUD today?

The Aussie has fallen for five straight weeks to lose nearly 5% over this period. This currency pair opened at 0.6211 to edge towards 0.6230 as Asian markets came online.

Central Bank Notes:

- The RBA kept the cash rate target unchanged at 4.35% on 10 December, marking the ninth consecutive pause.

- Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance. However, measures of underlying inflation are around 3.5%, which is still some way from the 2.5% midpoint of the inflation target.

The most recent forecasts published in the November Statement on Monetary Policy (SMP) do not see inflation returning sustainably to the midpoint of the target until 2026 but the Board is gaining some confidence that inflationary pressures are declining in line with these recent forecasts with risks remaining in place.

- Growth in output has been weak as the economy grew by only 0.8% in the September quarter over the past year. Outside of the COVID-19 pandemic, this was the slowest pace of growth since the early 1990s.

- A range of indicators suggest that labour market conditions remain tight; while those conditions have been easing gradually, some indicators have recently stabilised. The unemployment rate was 4.1 per cent in October, up from 3.5 per cent in late 2022.

- Wage pressures have eased more than expected in the November SMP. The rate of wages growth as measured by the Wage Price Index was 3.5% over the year to the September quarter, a step down from the previous quarter, but labour productivity growth remains weak.

- Sustainably returning inflation to target within a reasonable timeframe remains the Board’s highest priority. This is consistent with the RBA’s mandate for price stability and full employment. To date, longer term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

The Board will continue to rely upon the data and the evolving assessment of risks to guide its decisions, paying close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market.

- The next meeting is on 18 February 2025.

Next 24 Hours Bias

Weak Bullish

The Kiwi Dollar (NZD)

Key news events today

No major news events.

What can we expect from NZD today?

Just like its Pacific neighbour, the Kiwi has depreciated significantly as it tumbled 4.8% over the past four weeks. This currency pair opened at 0.5626 to drift higher at the beginning of the Asia session.

Central Bank Notes:

- The Monetary Policy Committee (MPC) agreed to reduce the Official Cash Rate (OCR) by 50 basis points bringing it down to 4.25% on 27 November, marking the third consecutive rate cut.

- The Committee assessed that annual consumer price inflation has declined and is now close to the midpoint of the MPC’s 1 to 3% target band; inflation expectations are also close to target and core inflation is converging to the midpoint.

- Economic activity remains subdued and output continues to be below its potential. With excess productive capacity in the economy, inflation pressures have eased. If economic conditions continue to evolve as projected, the Committee expects to be able to lower the OCR further early next year.

- Domestic economic activity remains below trend, as a result of weakness in demand for durable goods consumption and investment. This has been reflected in falling activity in interest rate sensitive sectors such as construction, manufacturing, and retail trade. In contrast, some services sectors have continued to grow.

- Consistent with feedback from business visits, high frequency indicators suggest that the economy has stabilised in recent months. Economic growth is expected to recover from the December quarter, in part due to lower interest rates, but there is uncertainty around the exact timing and speed of the recovery.

- Wage growth is slowing, consistent with inflation returning to the target midpoint while employment levels and job vacancies have declined, reflecting subdued economic activity; unemployment is expected to continue rising in the near term.

- Expectations of future inflation, the pricing intentions of firms, and spare productive capacity are consistent with the inflation target being sustainably achieved, providing the context and the confidence for the Committee to further ease monetary policy restraint.

- The next meeting is on 19 February 2025.

Next 24 Hours Bias

Weak Bullish

The Japanese Yen (JPY)

Key news events today

Manufacturing PMI (12:30 am GMT)

What can we expect from JPY today?

Japan’s manufacturing sector has remained in contraction since July with the final PMI reading of 49.6 for December indicating no change to this trend. This sector saw softer deterioration in manufacturing conditions at the end of 2024 as production and demand fell slower than expected while there was a renewed increase in employment. The yen remains weak keeping USD/JPY elevated – this currency pair was hovering around 157.80 by midday Asia.

Central Bank Notes:

- The Policy Board of the Bank of Japan decided on 19 December, by a 8-1 majority vote, to set the following guideline for money market operations for the intermeeting period:

- The Bank will encourage the uncollateralized overnight call rate to remain at around 0.25%.

- The Bank will embark on a plan to reduce the amount of its monthly outright purchases of JGBs so that it will be about 3 trillion yen in January-March 2026; the amount will be cut down by about 400 billion yen each calendar quarter in principle.

- Japan’s economy has recovered moderately, although some weakness has been seen in part. Exports and industrial production have been more or less flat while corporate profits have been on an improving trend and business sentiment has stayed at a favourable level.

- The employment and income situation has improved moderately while private consumption has been on a moderate increasing trend despite the impact of price rises and other factors.

- On the price front, the year-on-year rate of increase in the consumer price index (CPI, all items less fresh food) has been in the range of 2.0-2.5% recently, as services prices have continued to rise moderately, reflecting factors such as wage increases, although the effects of a passthrough to consumer prices of cost increases led by the past rise in import prices have waned; inflation expectations have risen moderately.

- With regard to the CPI (all items less fresh food), while the effects of the pass-through to consumer prices of cost increases led by the past rise in import prices are expected to wane, underlying CPI inflation is expected to increase gradually, since it is projected that the output gap will improve and that medium- to long-term inflation expectations will rise with a virtuous cycle between wages and prices continuing to intensify.

- Japan’s economy is likely to keep growing at a pace above its potential growth rate, with overseas economies continuing to grow moderately and as a virtuous cycle from income to spending gradually intensifies against the background of factors such as accommodative financial conditions.

- The next meeting is on 24 January 2025.

Next 24 Hours Bias

Weak Bearish

The Euro (EUR)

Key news events today

No major news events.

What can we expect from EUR today?

The Euro has tumbled nearly 1.3% over the last three weeks as it looks to re-test its 52-week low at 1.0331. This currency pair opened at 1.0426 and was edging higher towards 1.0440 as Asian markets came online.

Central Bank Notes:

- The Governing Council reduced the three key ECB interest rates by 25 basis points on 12 December to mark the third successive rate cut.

- Accordingly, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be decreased to 3.15%, 3.40% and 3.00% respectively.

- The disinflation process is well on track and most measures of underlying inflation suggest that inflation will settle at around the Governing Council’s 2% medium-term target on a sustained basis.

- Staff see headline inflation averaging 2.4% in 2024, 2.1% in 2025, 1.9% in 2026 and 2.1% in 2027 when the expanded EU Emissions Trading System becomes operational. For inflation excluding energy and food, staff project an average of 2.9% in 2024, 2.3% in 2025 and 1.9% in both 2026 and 2027.

- Staff now expect a slower economic recovery than in the September projections. Although growth picked up in the third quarter of this year, survey indicators suggest it has slowed in the current quarter – the economy is expected to grow by 0.7% in 2024, 1.1% in 2025, 1.4% in 2026 and 1.3% in 2027

- The Eurosystem no longer reinvests all of the principal payments from maturing securities purchased under the pandemic emergency purchase programme (PEPP), reducing the PEPP portfolio by €7.5 billion per month on average and the Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

- The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises sustainably at its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission.

- The next meeting is on 30 January 2025.

Next 24 Hours Bias

Weak Bullish

The Swiss Franc (CHF)

Key news events today

No major news events.

What can we expect from CHF today?

The franc has weakened significantly since the end of September with UDS/CHF rallying almost 7.5% over this period. This currency pair opened at 0.9010 before drifting lower at the beginning of the Asia session.

Central Bank Notes:

-The SNB eased monetary policy by lowering its key policy rate by 50 basis points, going from 1.00% to 0.50% on 12 December, marking for the fourth consecutive reduction.

Underlying inflationary pressure has decreased again this quarter.

- Inflation in the period since the last monetary policy assessment has again been lower than expected as it decreased from 1.1% in August to 0.7% in November; both goods and services contributed to this decline.

- In the shorter term, the new conditional inflation forecast is below that of September: 1.1% for 2024, 0.3% for 2025 and 0.8% for 2026, based on the assumption that the SNB policy rate is 0.5% over the entire forecast horizon.

- GDP growth in Switzerland was only modest in the third quarter of 2024 with growth in the services sector was again somewhat stronger, while value added in manufacturing declined.

- There was a further slight increase in unemployment, and employment growth was subdued while the utilisation of overall production capacity was

normal.

- The SNB anticipates GDP growth of around 1% this year while currently expecting growth of between 1.0% and 1.5% for 2025.

- The SNB will continue to monitor the situation closely, and will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term.

- The next meeting is on 20 March 2025.

Next 24 Hours Bias

Weak Bearish

The Pound (GBP)

Key news events today

No major news events.

What can we expect from GBP today?

Just like many other currencies, the Pound has devalued strongly in the last quarter of this year with Cable breaking under the threshold of 1.2500 on 20th December. This currency pair opened at 1.2572 and was hovering around this level as Asian markets came online.

Central Bank Notes:

- The Bank of England’s Monetary Policy Committee (MPC) voted by a majority of 6 to 3 to maintain the Bank Rate at 4.75% on 19 December 2024 – three members preferred to reduce the Bank rate by 25 basis points, bringing it down to 4.50%.

- The MPC also voted unanimously to reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100B over the next 12 months to a total of £558B, starting in October 2024. On 18 December 2024, the stock of UK government bonds held for monetary policy purposes was £655B.

- Twelve-month CPI inflation had increased to 2.6% in November from 1.7% in September, slightly higher than previous expectations while services consumer price inflation had remained elevated, at 5.0%, while core goods price inflation had risen to 1.1%.

- Headline CPI inflation was slightly higher than previous expectations, owing in large part to stronger inflation in core goods and food, and is expected to continue to rise slightly in the near term.

- Most indicators of UK near-term activity have declined with Bank staff expecting GDP growth to be weaker at the end of the year than originally projected in the November Monetary Policy Report.

- Bank staff now expected zero GDP growth in 2024 Q4, weaker than the 0.3% that had been incorporated in the November Report, broadly consistent with the latest combined steer from business surveys and the available official data.

- The Committee now judges that the labour market is broadly in balance as annual private sector regular average weekly earnings growth picked up quite sharply in the three months to October but there remains significant uncertainty around developments in the labour market.

- Monetary policy has been guided by the need to squeeze remaining inflationary pressures out of the economy to achieve the 2% target both in a timely manner and on a lasting basis. Over recent quarters there has been progress in disinflation, particularly as previous external shocks have abated, although remaining domestic inflationary pressures are resolving more slowly.

- The Committee continues to monitor closely the risks of inflation persistence and will assess the extent to which the evolving evidence is consistent with more constrained supply, which could sustain inflationary pressures, or with weaker demand, which could lead to the emergence of spare capacity in the economy and push down inflation; a gradual approach to removing monetary policy restraint remains appropriate.

- Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further and the Committee will decide the appropriate degree of monetary policy restrictiveness at each meeting.

- The next meeting is on 6 February 2025.

Next 24 Hours Bias

Weak Bullish

The Canadian Dollar (CAD)

Key news events today

No major news events.

What can we expect from CAD today?

The Loonie has been one of the weakest currencies in 2024 causing USD/CAD to surge beyond 1.4450 in recent weeks. This currency pair opened at 1.4413 and is likely to remain elevated as the day progresses.

Central Bank Notes:

- The Bank of Canada reduced its target for the overnight rate by 50 basis points bringing it down to 3.25% while continuing its policy of balance sheet normalization on 11 December; this marked the fifth consecutive meeting where rates were reduced.

- Canada’s economy grew by 1% in the third quarter, somewhat below the Bank’s October projection, and the fourth quarter also looks weaker than projected. Third-quarter GDP growth was pulled down by business investment, inventories and exports.

- The unemployment rate rose to 6.8% in November as employment continued to grow more slowly than the labour force while wage growth showed some signs of easing, but remains elevated relative to productivity.

- Headline CPI has declined significantly from 2.7% in June to 1.6% in September while shelter costs inflation remains elevated but has begun to ease; the preferred measures of core inflation are now below 2.5%.

- CPI inflation has been about 2% since the summer, and is expected to average close to the 2% target over the next couple of years. Since October, the upward pressure on inflation from shelter and the downward pressure from goods prices have both moderated as expected.

- Looking ahead, the GST holiday will temporarily lower inflation but that will be unwound once the GST break ends. In addition, the possibility the incoming US administration will impose new tariffs on Canadian exports to the United States has increased uncertainty and clouded the economic outlook

- With inflation around 2%, the economy in excess supply, and recent indicators tilted towards softer growth than projected, the Governing Council decided to reduce the policy rate by a further 50 basis points to support growth and keep inflation close to the middle of the 1-3% target range.

- The Governing Council has reduced the policy rate substantially since June and going forward, they will be evaluating the need for further reductions in the policy rate one decision at a time.

- The Bank is committed to maintaining price stability for Canadians by keeping inflation close to the 2% target.

- The next meeting is on 29 January 2025.

Next 24 Hours Bias

Weak Bullish

Oil

Key news events today

No major news events.

What can we expect from Oil today?

After Friday’s larger-than-expected drawdown in the EIA inventories, crude oil prices are likely to remain buoyed on Monday. WTI oil was hovering around $70.50 per barrel as markets re-opened and this benchmark could continue its upward ascent towards the $72-mark.

Next 24 Hours Bias

Weak BullishTuesday 10th December 2024: Asian Markets Rally Amid China’s Stimulus Plans

By IC Markets

Global Markets:

Asian Stock Markets : Nikkei up 0.53%, Shanghai Composite up 1.22%, Hang Seng up 0.87% ASX down 0.36%

Commodities : Gold at $2691.35 (0.14%), Silver at $32.4 (-0.18%), Brent Oil at $71.4 (-0.46%), WTI Oil at $67.7 (-0.49%)

Rates : US 10-year yield at 4.193, UK 10-year yield at 4.2705, Germany 10-year yield at 2.1175

News & Data:

(USD) Final Wholesale Inventories m/m 0.2% vs 0.2% expected

Markets Update:

China’s stock markets rose on Tuesday, with the CSI 300 index gaining 1.9% and Hong Kong’s Hang Seng index up 0.9%, driven by Beijing’s announcement of “more proactive” fiscal policies and “moderately” looser monetary measures for the upcoming year. These changes aim to stimulate domestic consumption and were revealed in an official statement on Monday evening, which had already propelled the Hang Seng nearly 3% higher.

Elsewhere in Asia, South Korea’s Kospi surged 2.2%, while the small-cap Kosdaq soared 5.3%, with investors monitoring political developments. Yonhap reported that opposition leader Lee Jae Myung committed to passing a scaled-down budget later in the day. Meanwhile, Japan’s Nikkei 225 and Topix rose 0.52% and 0.37%, respectively. However, Australia’s S&P/ASX 200 dipped 0.36% after the Reserve Bank of Australia maintained its benchmark rate at 4.35%.

In the U.S., Wall Street retreated on Monday ahead of critical inflation data. The S&P 500 fell 0.61% to 6,052.85, the Nasdaq lost 0.62% to 19,736.69, and the Dow Jones declined 0.54%, closing at 44,401.93. Technology stocks, including Nvidia and AMD, faced significant declines. Nvidia dropped 2.6% after facing an antitrust investigation in China, while AMD fell 5.6%. Tech giants Meta and Netflix also saw losses.

Upcoming Events:

01:30 PM GMT – USD Revised Nonfarm Productivity q/q

01:30 PM GMT – USD Revised Unit Labor Costs q/q

Global Markets:

Asian Stock Markets : Nikkei up 0.53%, Shanghai Composite up 1.22%, Hang Seng up 0.87% ASX down 0.36%

Commodities : Gold at $2691.35 (0.14%), Silver at $32.4 (-0.18%), Brent Oil at $71.4 (-0.46%), WTI Oil at $67.7 (-0.49%)

Rates : US 10-year yield at 4.193, UK 10-year yield at 4.2705, Germany 10-year yield at 2.1175

News & Data:

(USD) Final Wholesale Inventories m/m 0.2% vs 0.2% expected

Markets Update:

China’s stock markets rose on Tuesday, with the CSI 300 index gaining 1.9% and Hong Kong’s Hang Seng index up 0.9%, driven by Beijing’s announcement of “more proactive” fiscal policies and “moderately” looser monetary measures for the upcoming year. These changes aim to stimulate domestic consumption and were revealed in an official statement on Monday evening, which had already propelled the Hang Seng nearly 3% higher.

Elsewhere in Asia, South Korea’s Kospi surged 2.2%, while the small-cap Kosdaq soared 5.3%, with investors monitoring political developments. Yonhap reported that opposition leader Lee Jae Myung committed to passing a scaled-down budget later in the day. Meanwhile, Japan’s Nikkei 225 and Topix rose 0.52% and 0.37%, respectively. However, Australia’s S&P/ASX 200 dipped 0.36% after the Reserve Bank of Australia maintained its benchmark rate at 4.35%.

In the U.S., Wall Street retreated on Monday ahead of critical inflation data. The S&P 500 fell 0.61% to 6,052.85, the Nasdaq lost 0.62% to 19,736.69, and the Dow Jones declined 0.54%, closing at 44,401.93. Technology stocks, including Nvidia and AMD, faced significant declines. Nvidia dropped 2.6% after facing an antitrust investigation in China, while AMD fell 5.6%. Tech giants Meta and Netflix also saw losses.

Upcoming Events:

01:30 PM GMT – USD Revised Nonfarm Productivity q/q

01:30 PM GMT – USD Revised Unit Labor Costs q/qMonday 9th December 2024: Markets React to South Korea’s Political Unrest

By IC Markets

Global Markets:

Asian Stock Markets : Nikkei up 0.07%, Shanghai Composite down 0.14%, Hang Seng down 0.57% ASX up 0.02%

Commodities : Gold at $2659.35 (-0.14%), Silver at $31.4 (-0.48%), Brent Oil at $71.4 (0.46%), WTI Oil at $67.27 (0.49%)

Rates : US 10-year yield at 4.143, UK 10-year yield at 4.275, Germany 10-year yield at 2.1125

News & Data:

(USD) Non – Farm Employment Change 227K vs 218K expected

(USD) Unemployment Rate 4.2% vs 4.1% expected

(CAD) Employment Change 50.5K vs 24.7K expected

(CAD) Unemployment Rate 6.8% vs 6.6% expected

Markets Update:

South Korea’s Kospi index fell over 2% on Monday as political turmoil continued to weigh on investor sentiment following President Yoon Suk Yeol’s survival of an impeachment vote over the weekend. The benchmark Kospi dropped 2.5%, while the Kosdaq slid 4.4%, reflecting heightened concerns over the fallout from Yoon’s brief declaration of martial law. Adding to the tension, prosecutors have reportedly named Yoon as a subject of a criminal investigation for potential charges of treason and abuse of power.

The impeachment vote, led by opposition parties, was boycotted by Yoon’s People Power Party. However, the party’s leader has suggested that Yoon may consider stepping down, signaling further uncertainty in the political landscape. This development has fueled apprehension in the markets, with investors closely watching how the crisis unfolds.

Elsewhere in Asia-Pacific markets, performance was mixed. Japan’s Nikkei 225 inched up 0.1%, while the Topix added 0.2%, supported by a positive revision to Japan’s third-quarter GDP growth, now estimated at 0.3% quarter-on-quarter. Meanwhile, Hong Kong’s Hang Seng index dropped 0.6%, and mainland China’s CSI 300 declined 0.5%. China’s consumer price growth in November missed expectations, rising only 0.2% year-on-year compared to 0.3% in October, according to the National Bureau of Statistics.

In the U.S., markets ended last week on a high note. The S&P 500 gained 0.25% to 6,090.27, and the Nasdaq Composite climbed 0.81% to 19,859.77, bolstered by gains in Tesla, Meta Platforms, and Amazon. However, the Dow Jones Industrial Average dipped 0.28%, closing at 44,642.52. Both the S&P 500 and Nasdaq achieved their third consecutive week of gains, rising 0.96% and 3.34%, respectively, despite the Dow slipping 0.6% over the same period.

Upcoming Events:

03:00 PM GMT – USD Final Wholesale Inventories m/m

Global Markets:

Asian Stock Markets : Nikkei up 0.07%, Shanghai Composite down 0.14%, Hang Seng down 0.57% ASX up 0.02%

Commodities : Gold at $2659.35 (-0.14%), Silver at $31.4 (-0.48%), Brent Oil at $71.4 (0.46%), WTI Oil at $67.27 (0.49%)

Rates : US 10-year yield at 4.143, UK 10-year yield at 4.275, Germany 10-year yield at 2.1125

News & Data:

(USD) Non – Farm Employment Change 227K vs 218K expected

(USD) Unemployment Rate 4.2% vs 4.1% expected

(CAD) Employment Change 50.5K vs 24.7K expected

(CAD) Unemployment Rate 6.8% vs 6.6% expected

Markets Update:

South Korea’s Kospi index fell over 2% on Monday as political turmoil continued to weigh on investor sentiment following President Yoon Suk Yeol’s survival of an impeachment vote over the weekend. The benchmark Kospi dropped 2.5%, while the Kosdaq slid 4.4%, reflecting heightened concerns over the fallout from Yoon’s brief declaration of martial law. Adding to the tension, prosecutors have reportedly named Yoon as a subject of a criminal investigation for potential charges of treason and abuse of power.

The impeachment vote, led by opposition parties, was boycotted by Yoon’s People Power Party. However, the party’s leader has suggested that Yoon may consider stepping down, signaling further uncertainty in the political landscape. This development has fueled apprehension in the markets, with investors closely watching how the crisis unfolds.

Elsewhere in Asia-Pacific markets, performance was mixed. Japan’s Nikkei 225 inched up 0.1%, while the Topix added 0.2%, supported by a positive revision to Japan’s third-quarter GDP growth, now estimated at 0.3% quarter-on-quarter. Meanwhile, Hong Kong’s Hang Seng index dropped 0.6%, and mainland China’s CSI 300 declined 0.5%. China’s consumer price growth in November missed expectations, rising only 0.2% year-on-year compared to 0.3% in October, according to the National Bureau of Statistics.

In the U.S., markets ended last week on a high note. The S&P 500 gained 0.25% to 6,090.27, and the Nasdaq Composite climbed 0.81% to 19,859.77, bolstered by gains in Tesla, Meta Platforms, and Amazon. However, the Dow Jones Industrial Average dipped 0.28%, closing at 44,642.52. Both the S&P 500 and Nasdaq achieved their third consecutive week of gains, rising 0.96% and 3.34%, respectively, despite the Dow slipping 0.6% over the same period.

Upcoming Events:

03:00 PM GMT – USD Final Wholesale Inventories m/mFriday 1st November 2024: Asia-Pacific Markets Slide Following Wall Street Losses Amid Economic Unce

By IC Markets

IC Markets Global • Nov 1, 2024

IC Markets Europe Fundamental Forecast | 21 October 2024

By IC Markets

What happened in the Asia session?

Although RBA Deputy Governor Andrew Hauser comments in a fireside chat at the Commonwealth Bank of Australia Global Markets Conference in Sydney were hawkish, the Aussie reversed sharply from 0.6716 to break under 0.6700 to drop as low as 0.6687 this morning. Deputy Governor Hauser stated that “inflation is still too high and rates are unlikely to be cut in 2024”, reaffirming the RBA’s dual mandate of keeping prices stable between 2 and 3% while also supporting full employment. Persistent demand for the greenback is keeping the overhead pressures firm in place for the Aussie and this current downward momentum is likely to extend even lower today.

What does it mean for the Europe & US sessions?

There are not one but three Federal Reserve officials delivering their respective speeches in the latter part of the day. Federal Reserve Bank of Dallas President Lorie Logan will be participating in a moderated discussion at the Securities Industry and Financial Markets Association Annual Meeting in New York while Minneapolis President Neel Kashkari will be speaking at the Chippewa Falls Chamber of Commerce where audience questions are expected. And finally, Kansas City President Jeffrey Schmid speaks about the economic outlook and monetary policy at the Chartered Financial Analysts Society in Kansas City where audience questions are also expected. These events are likely to inject higher volatility for financial markets as the U.S. session commences.

The Dollar Index (DXY)

Key news events today

FOMC Member Logan Speaks (12:55 pm GMT)

FOMC Member Kashkari Speaks (5:00 pm GMT)

FOMC Member Schmid Speaks (9:05 pm GMT)

What can we expect from DXY today?

There are not one but three Federal Reserve officials delivering their respective speeches in the latter part of the day. Federal Reserve Bank of Dallas President Lorie Logan will be participating in a moderated discussion at the Securities Industry and Financial Markets Association Annual Meeting in New York while Minneapolis President Neel Kashkari will be speaking at the Chippewa Falls Chamber of Commerce where audience questions are expected. And finally, Kansas City President Jeffrey Schmid speaks about the economic outlook and monetary policy at the Chartered Financial Analysts Society in Kansas City where audience questions are also expected. These events are likely to inject higher volatility for financial markets as the U.S. session commences.

Central Bank Notes:

The Federal Funds Rate target range was reduced by 50 basis points to 4.75% to 5.00% on 18th September in an 11 to 1 vote with Governor Michelle Bowman dissenting, preferring to cut rates by a smaller amount.

The Committee seeks to achieve maximum employment and inflation at the rate of 2% over the longer run and has gained greater confidence that inflation is moving sustainably toward 2%, and judges that the risks to achieving its employment and inflation goals are roughly in balance.

The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

Recent indicators suggest that economic activity has continued to expand at a solid pace while job gains have slowed, and the unemployment rate has moved up but remains low.

Inflation has made further progress toward the Committee’s 2% objective but remains somewhat elevated.